Global shares surged in the past week to new record highs in the US, Europe and Japan, helped in particular by enthusiasm for Artificial Intelligence after a very strong earnings result from AI chip maker Nvidia which served to offset ongoing indications from central banks that they will not be rushing to cut interest rates. For the week US and Eurozone shares rose 1.7%. Japanese shares rose 1.6% and finally made it past their 29 December 1989 bubble years high, after a long recovery from a 20-year 82% slump into their 2009 low. Chinese shares rose 3.7% with ongoing share market support measures. Despite the positive global lead Australian shares fell 0.2% for the week – reflecting the reality that the local market does not have much exposure to AI stocks and saw mixed earnings results – with gains in IT and utilities shares offset by falls in resources, property and consumer staple stocks. Bond yields generally fell globally and were flat in Australia. Metal prices rose but oil and iron ore prices fell and the $A rose with a fall in the $US.

The past week saw more indications from major central banks that they are not rushing into rate cuts.

- The minutes from the last Fed meeting reiterated that its seeing progress in reducing inflation but wants more evidence that it will be sustained and is wary about moving too quickly to cut rates with stronger economic activity data lately providing them with flexibility. Speeches by Fed officials tended to back this up.

- The minutes from the last ECB meeting echoed a similar sentiment with disinflation seen as proceeding but a wariness of cutting rates too early with a still robust labour market.

- And in Australia, the minutes from the last RBA Board meeting repeated that the RBA now sees the risks to the outlook as being more balanced and its more confident that inflation will fall back to target but so far its not sufficiently confident and as at the last meeting was still only considering hiking again or holding but not yet considering a rate cut. As such it clearly retains a mild tightening bias whereas the Fed and ECB are more neutral.

There is nothing new in any of this, but it reminds us that we still have a way to go in terms of actually seeing rate cuts and market expectations have consequently become more tempered as a result. And reflecting the lag in inflation in Australia compared to other countries, the RBA is not surprisingly still lagging the Fed and will likely do so when it comes to starting to cut rates. That said the broader picture globally remains one of falling inflation with Canada being the latest to see another fall in underlying inflation in January. While the road to lower inflation is likely to remain bumpy, we continue to see sufficient progress such that the Fed and ECB will cut rates around five times this year starting in the June quarter and the RBA will cut by around three times starting mid-year. We would concede through that the risk in Australia is that the cuts could start a bit later around August/September.

Source: Bloomberg, AMP

Share markets so far have largely been able to look through the push back from central banks against early rate cuts helped by a combination of solid US economic data, enthusiasm for AI which is continuing to boost US tech stocks, good earnings results in the US and better than feared earnings results in Australia and expectations that rate cuts are still on the way and when they come they might be “good news cuts” (reflecting lower inflation) rather than “bad news cuts” (reflecting recession). As a result, while shares have become vulnerable after their surge since last October’s lows so far any pull backs have been brief and the trend has remained up.

There are still plenty of possible triggers for a correction in shares – rate cut delays, high geopolitical and recession risks and soft seasonality around this time of year. And the enthusiasm around AI is now getting a bit frothy along with general investor sentiment which leaves shares a bit vulnerable to any bad news. However, we continue to see the broad trend as up for global and Australian shares this year as rates fall and recession is ultimately avoided or if not then its mild.

Comparisons are being made between the AI boom today and the tech bubble of the late 1990s but there are big differences in that AI related tech companies are seeing strong earnings growth (Nvidia’s earnings are up 486%yoy) and while the forward PE on Nasdaq today is high at 32 times, it’s not the 100 times plus it was at the tech bubble high in 2000. Investors do need to be wary though about jumping on the AI bandwagon as related chip making is highly competitive, it will take time for the economic benefits of AI to be realised and the real winners may turn out to be different to today’s highflyers as occurred with many tech stocks a generation ago.

Economic activity trackers

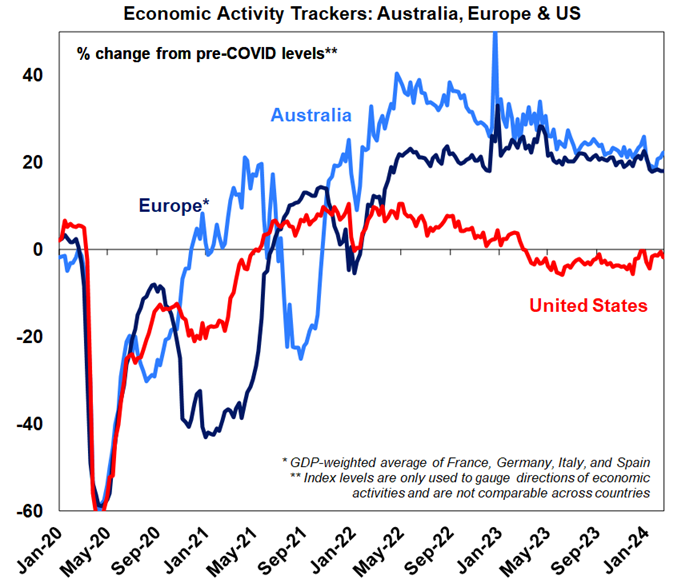

Our Economic Activity Trackers have bounced back a bit in Australia, but are still not showing anything decisive.

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence and credit & debit card transactions. Source: AMP

Major global economic events and implications

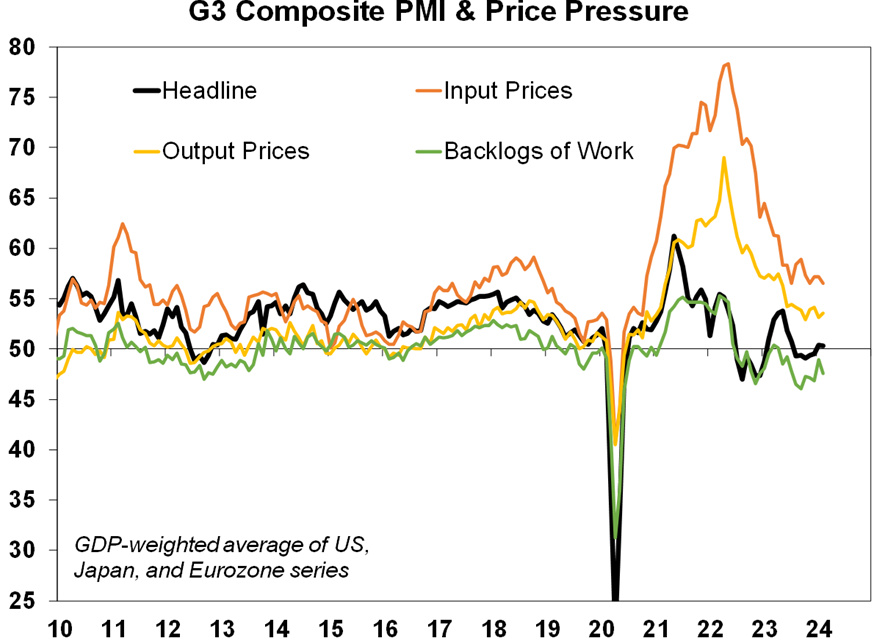

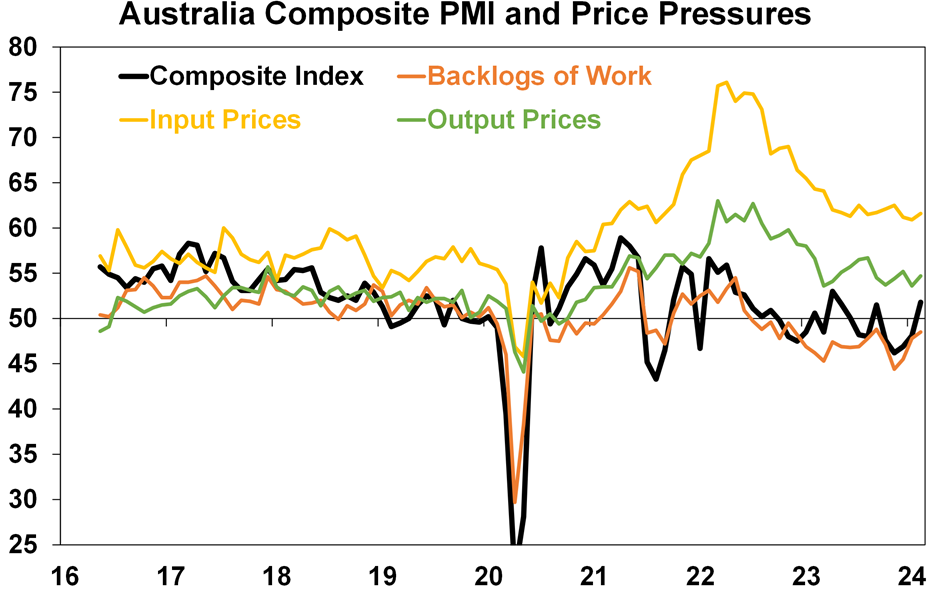

February business conditions PMIs (which are global surveys of businesses) were mixed across major countries – up in Europe (but still soft), the UK and Australia but down in the US and Japan (but to still okay levels). Across the G3 as a whole they were little changed. G3 input prices edged down while output prices edged up with both well down from their highs and around 2018 levels with order backlogs continuing to fall and delivery times improving slightly (despite shipping issues).

Source: Bloomberg, AMP

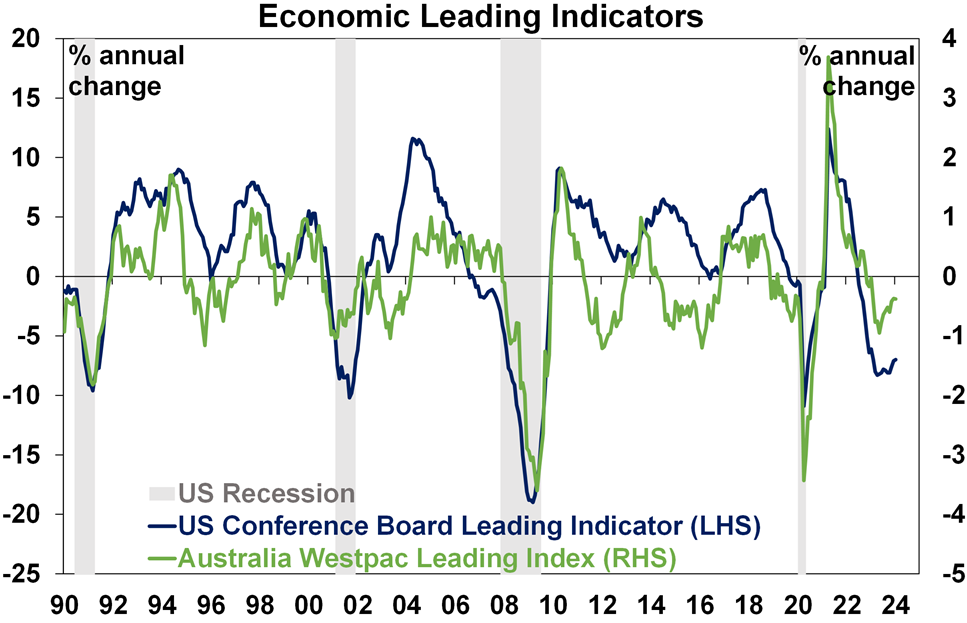

US economic existing home sales rose in January and jobless claims remain very low. The US leading index fell again in the last week but its been edging away from levels normally associated with recession with The Conference Board, which provides the index, now reportedly dropping its US recession forecast. Interestingly Australia’s leading indicator never fell as far as around the early 1990s recession, the GFC and in 2020 and it’s now becoming less negative. On the inflation front the output price component in the US PMI is around its average levels seen last decade.

Source: Bloomberg, AMP

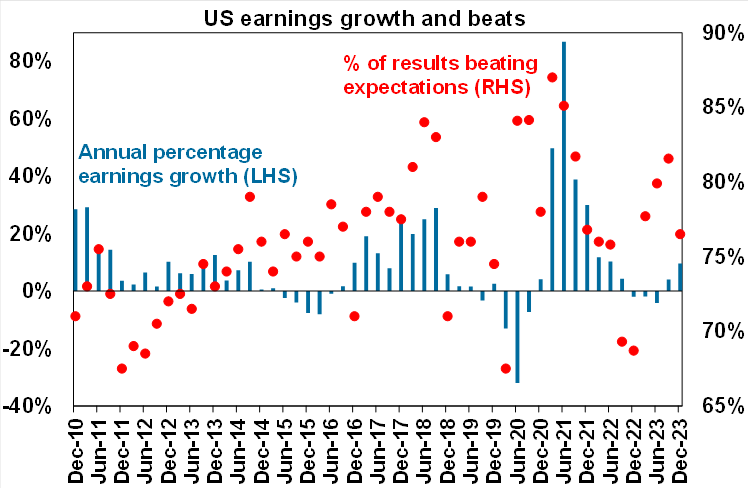

Around 90% of US S&P 500 companies have now reported December quarter earnings with 76.5% coming in better than expected, which is just above the norm of 76%. Earnings growth for the quarter is running around +9.6%yoy, which is well up from consensus expectations for 4.3% growth at the start of the reporting season. Earnings growth has been driven by technology companies (+40%) and financials (+11%) with resources earnings down 21%.

Source: Bloomberg, UBS, AMP

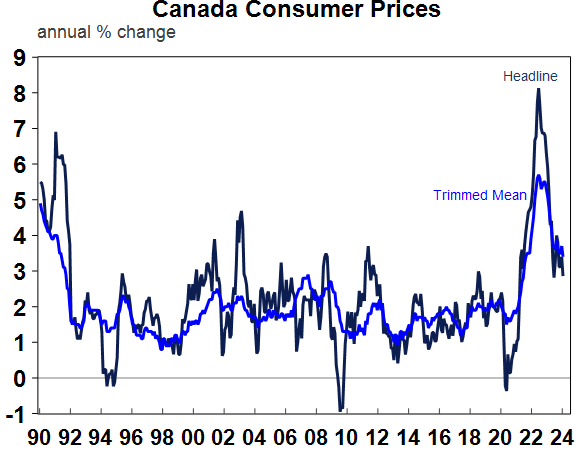

Canadian inflation fell more than expected to 2.9%yoy in January with underlying measures of inflation also down to around 3.4%yoy. The BoC is likely on track to start cutting rates in the September quarter.

Source: Macrobond, AMP

A rise in the Eurozone composite PMI for February is consistent with a slight improvement in growth this quarter.

The People’s Bank of China cut it’s 5-year prime lending rate by 0.25% to 3.95%. A cut had long been expected but the size was greater than normal reflecting a desire to boost the property market as the 5 year lending rate is the reference rate for mortgage rates. With confidence amongst property buyers so depressed though its unclear whether it will be enough. Home prices continued to fall in January. Meanwhile total domestic tourism spending over the Chinese New Year holiday period looks to have surged relative to the 2023 holiday period which is a positive sign but there are some reasons for caution in interpreting this: it may have come at the expense of spending on goods; 2023 was a low base as it was impacted by the Covid lockdowns; the 2024 holiday was effectively a bit longer than that in 2023; and the 2024 holiday included Valentine’s Day which is widely celebrated in China whereas the 2023 holiday did not.

Australian economic events and implications

Australian business conditions PMIs for February rose with strength in services (possibly driven by optimism regarding a boost from Swiftonomics this month) but for the last 18 months they have been range bound around zero. While work backlogs continue to fall, a concern though is that the fall in input and output prices appears to have stabilised for now at higher than pre-pandemic levels particularly for services input prices. This likely reflects the pick-up in wages growth.

Source: Bloomberg, AMP

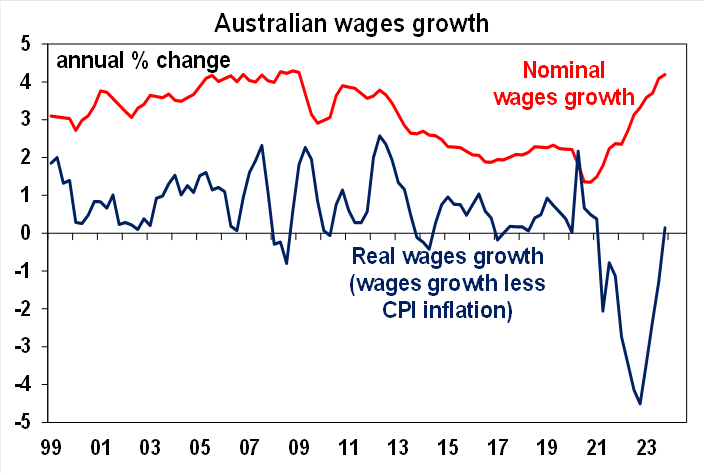

Annual wages growth in the December quarter at 4.2%yoy rose to its fastest pace since 2009 resulting in the first rise in real wages since 2021. The rise in real wages was only just 0.1% but with inflation likely to slow further relative to wages growth we expect real wage growth to be running around +0.5% by year end. Thanks to revisions to past data this was slightly stronger than RBA and market expectations for a 4.1%yoy increase.

Source: Bloomberg, AMP

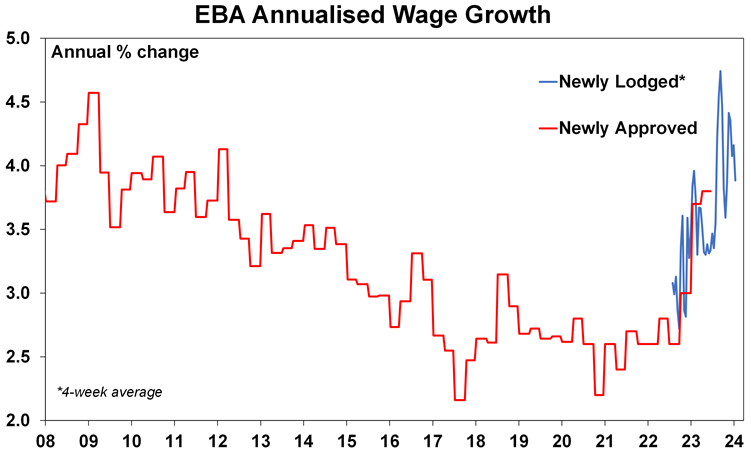

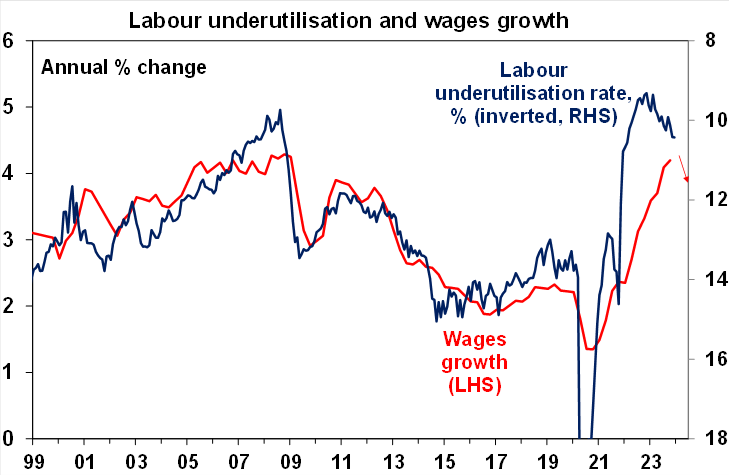

However, this is likely to be the peak in wages growth: the quarterly pace slowed to 0.9%qoq which was in line with expectations; while public wages growth picked up owing to changes to state government wage policies and a pay rise for aged care workers, private wages growth slowed; wage increases including bonuses which led on the way up look to have peaked; wage increases under enterprise bargaining agreements look to have peaked (see the first chart below); and the cooling jobs market points to slowing wages growth ahead (second chart below). Wages growth in Australia also remains below that in the US, UK and Europe. All up we don’t see the latest wages data altering the outlook for interest rates in Australia.

Source: DEWR; AMP

Source: Bloomberg, AMP

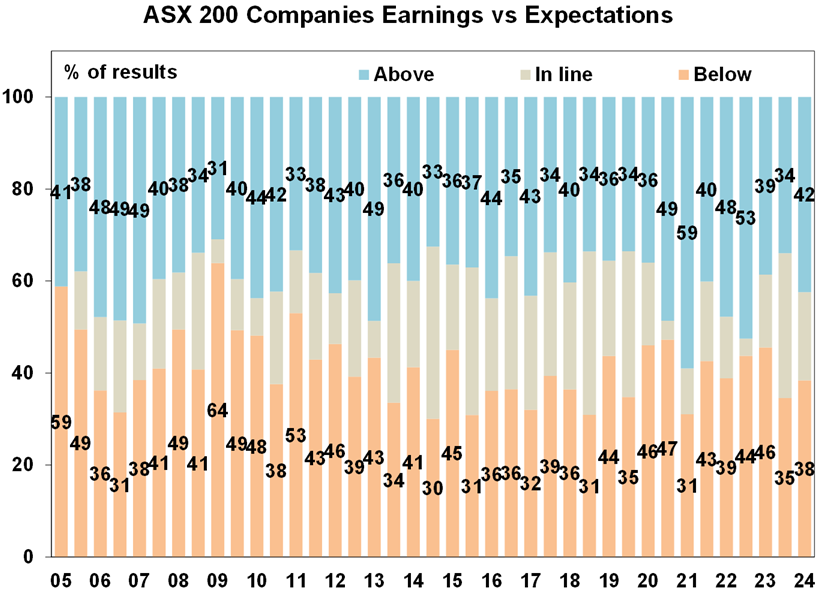

The Australian December half earnings reporting season is nearly 80% complete and its now looking rather average. After the usual run of better results to start with its now tailed off a bit with the level of companies beating earnings expectations falling over the last week although it’s still fractionally better than average. Consensus expectations remain for a -5.5% fall in profits this financial year (down from -4.9% a month ago) with a big fall in energy sector profits on the back of lower oil, coal and gas prices and small fall in bank profits but most other sectors seeing flat to up profits. The bad news has been that revenue growth is slowing and high interest expenses remain a problem, but the good news has been that the peak in cost growth may be near, labour market pressure appears to be starting to normalise, cost control remains strong and guidance has been stable.

- Beats have continued to exceed misses although the gap has now narrowed with 42% of results having surprised consensus earnings expectations on the upside and 38% surprising on the downside, which is only just a bit better than the long-term average for both of around 41%.

Source: Bloomberg, AMP

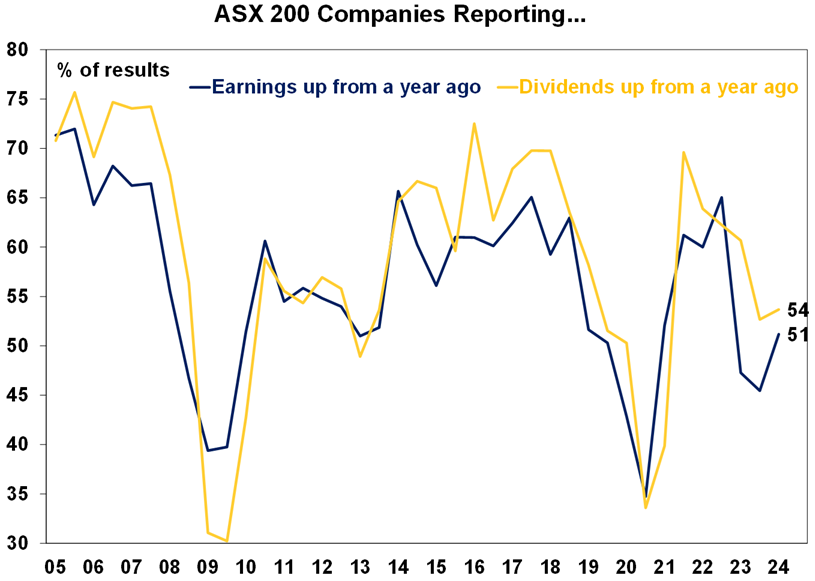

- 51% of companies have seen earnings rise from a year ago which is below the norm of 56% which is consistent with aggregate earnings being likely to fall this financial year, albeit the falls are concentrated in energy stocks.

- 54% of companies have increased their dividends on a year ago which is up a bit from last week but it’s below the norm of 59% and a greater than usual 32% have cut their dividends, which overall suggests a degree of caution.

Source: Bloomberg, AMP

What to watch over the next week?

In the US, the focus is likely to be on January core private final consumption inflation data (Thursday) which like the CPI is expected to rise 0.4%mom but fall to 2.8%yoy from 2.9%yoy in December. Personal spending growth in January is likely to have slowed to 0.2%mom from 0.7%, partly due to bad weather. In other data expect a fall in durable goods orders, unchanged consumer confidence and a further rise in home prices (Tuesday) and an unchanged ISM manufacturing conditions index at a still weak reading of 49.1 for February (Friday). The US Congress also needs to see progress on a spending package to pass a Continuing Resolution extending spending authorisations in order to avoid a partial government shutdown from 1 March.

Eurozone inflation data for February is likely to fall to 2.5%yoy from 2.8%yoy with unemployment unchanged at 6.4% (Friday).

Japanese inflation data for January (Tuesday) is likely to show a sharp fall to around 1.9%yoy with core inflation falling to around 2.4%yoy. Data for industrial production and retail sales (Thursday) and the labour market (Friday) will also be released.

Chinese business conditions PMIs for February (Friday) are likely to have remained subdued.

The Reserve Bank of New Zealand (Wednesday) is expected to leave its cash rate on hold at 5.5%.

In Australia, we expect the January ABS CPI (Wednesday) to fall 0.2%mom due to lower travel and fuel prices but the annual rate to rise slightly to 3.5%yoy (from 3.4%yoy) due to a base effect from a bigger monthly fall dropping out a year ago. Abstracting from the monthly volatility this should confirm the ongoing downtrend in inflation and progress towards rate cuts but on its own probably won’t be enough for the RBA to drop its mild tightening bias at its March meeting. In other data, expect a 0.6%qoq rise in December quarter construction spending (Wednesday). December quarter business investment is expected to show a 0.7% fall and point to a slowing in business investment growth this financial year, January retail sales are expected to rise 2% after the sharp fall in December partly reflecting seasonal adjustment problems and credit growth is likely to have remained moderate (all due Thursday). CoreLogic data for February are likely to show a 0.6% gain in Australian home prices (Friday), up from 0.4% in January, as the prospect of rate cuts ahead and the shortage of supply continue to offset the negative impact of high mortgage rates.

The Australian December half earnings reporting season will wrap up with 40 major companies reporting including NIB and Suncorp (Monday), Coles and Woodside (Tuesday), Worley (Wednesday) and Harvey Norman, Ramsay Health and Southern Cross Media (Thursday).

Outlook for investment markets for 2024

Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025 should make for okay investment returns this year. However, with shares historically tending to fall during the initial phase of rate cuts, a very high risk of recession and investors and share market valuations no longer positioned for recession and geopolitical risks, it’s likely to be a rougher and more constrained ride than in 2023.

Global shares are expected to return a far more constrained 7%. The first half could be rough as growth weakens and possibly goes negative and valuations are less attractive than a year ago, but shares should ultimately benefit from rate cuts, lower bond yields and the anticipation of stronger growth later in the year and in 2025.

Australian shares are likely to outperform global shares, after underperforming in 2023 helped by somewhat more attractive valuations. A recession could threaten this though so it’s hard to have a strong view. Expect the ASX 200 to return 9% in 2024 and rise to around 7900.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows and central banks cut rates.

Unlisted commercial property returns are likely to be negative again due to the lagged impact of high bond yields & working from home.

Australian home prices are likely to have a tougher year as still high interest rates constrain demand again and unemployment rises. The supply shortfall should provide support though and rate cuts from mid-year should help boost price gains later in the year.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.72, due to a fall in the overvalued $US & the Fed moving to cut rates earlier and by more than the RBA.

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.